Options hedging is defined as the practice of using options contracts to limit financial losses from adverse price movements in assets a business holds or plans to acquire. The industry term is "options hedging," and it sits within the broader discipline of financial risk management. Business professionals use put options, call options, strike prices, and expiration dates to set a predefined floor or ceiling on an asset's value. This guide covers options hedging explained for business owners and professionals, walking through the core strategies, cost drivers, the Greeks, and the most common mistakes that cost companies money.

What are the main types of options hedging strategies used by businesses?

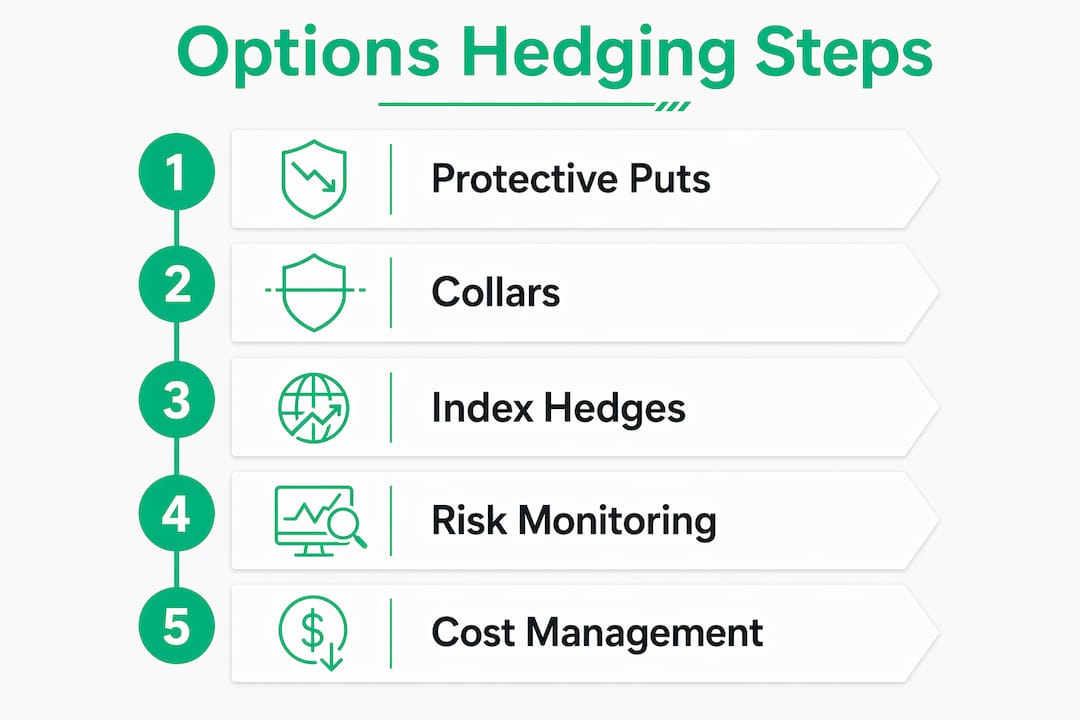

The three most widely used business options strategies are protective puts, collars, and portfolio-level index hedges. Each one solves a different problem, and each carries a different cost and trade-off.

Protective puts

A protective put gives a business the right to sell an asset at a fixed strike price before the option expires. Buying a put option effectively sets a floor under the position. If the stock or asset drops below the strike, the put gains value and offsets the loss. Think of it as paying an insurance premium: you spend money upfront, and you collect if the worst happens.

Collars

A collar combines a protective put with a covered call on the same underlying asset. The covered call generates premium income that offsets the cost of the put. A collar strategy can receive upfront premium, for example $3.65 per share, which directly reduces what the business pays for downside protection. The trade-off is a cap on upside gains. If the asset rallies past the call's strike price, the business does not participate in those gains.

Portfolio-level index hedges

Larger businesses with diversified holdings often use index options to hedge a basket of stocks at once rather than hedging each position individually. Index hedges work best when the portfolio's holdings move closely with the index being used. If the correlation (measured by Beta or R²) is low, the hedge may not fully protect against sector-specific losses. This approach is cost-efficient but requires careful correlation analysis before implementation.

Pro Tip: Start with a protective put on your single largest position before attempting a collar or index hedge. Mastering one structure on a small position teaches you more than reading about all three.

How do options hedging costs and timing affect business decisions?

Premium cost is the central financial variable in any hedging decision. Three factors drive what a business pays for an option:

- Implied volatility. Higher perceived market risk means higher premiums. A business hedging before an earnings announcement will pay more than one hedging during a quiet period.

- Time to expiration. Longer-dated options cost more but provide more coverage duration. Shorter-term options are cheaper but demand more accurate timing.

- Strike price distance. An at-the-money put costs more than a deep out-of-the-money put because it provides immediate protection.

Options are typically purchased with expiration dates 30–60 days out. That window balances premium cost against hedge duration. Going shorter saves money but increases the risk of the hedge expiring before the threat passes. Going longer locks in more protection but raises the upfront cost significantly.

Time decay, known as theta, works against the option buyer every day. An option loses a portion of its value simply by sitting there, even if the underlying asset does not move. Businesses that buy protection and then ignore it often find the option has decayed to near zero before any market event occurs.

Pro Tip: When implied volatility spikes, option premiums spike with it. If you need a hedge, buy it during calm markets. Waiting until volatility is already elevated means paying a premium for protection that may already be partially priced in.

How can business owners use the Greeks to manage risk in options hedging?

The Greeks are a set of metrics that measure how an option's price responds to changes in the market. The Greeks, including Delta, Gamma, Theta, and Vega, are the core tools for monitoring and adjusting a hedge in real time. Ignoring them is like driving without a dashboard.

- Delta measures how much the option's price moves for every $1 move in the underlying asset. A delta of 0.50 means the option gains $0.50 for every $1 the stock rises. Businesses use delta to size hedges correctly relative to their exposure.

- Gamma measures how fast delta itself changes as the asset price moves. High gamma means the hedge's effectiveness can shift quickly, requiring more frequent adjustment.

- Theta measures daily time decay. Every day that passes, theta erodes the option's value. A business holding a protective put must weigh this ongoing cost against the protection it receives.

- Vega measures sensitivity to changes in implied volatility. A long put gains value when volatility rises, which is typically when markets fall. That relationship is what makes puts effective as a hedge.

Maintaining a delta-neutral portfolio reduces directional exposure by balancing the net delta of all positions near zero. A business with a large long stock position can buy puts with a combined negative delta that offsets the stock's positive delta. The result is a portfolio that does not gain or lose significantly from small price moves in either direction.

Effective risk management requires active monitoring of the Greeks and adjusting positions as market conditions change. A hedge that was delta-neutral on Monday may be significantly off by Friday if the underlying asset has moved sharply. Businesses that treat hedges as set-and-forget structures consistently underperform those that monitor and rebalance.

Pro Tip: Check your portfolio's net delta at least weekly. A hedge that drifts far from delta-neutral is no longer doing its job, and you may be paying theta for protection that has already eroded.

When and why should businesses implement options hedging?

Hedging is most effective in three specific business situations. Knowing when to hedge matters as much as knowing how.

- Protecting unrealized gains. A business that holds a stock position sitting on significant paper profits faces a dilemma. Selling triggers a capital gains tax event. Hedging with a protective put or collar preserves the gain without forcing a sale, giving the business time to plan the exit.

- Before binary events. Earnings announcements, regulatory decisions, and Federal Reserve rate decisions can move markets sharply in either direction. Buying protection before these events limits the damage if the outcome is negative.

- Managing concentrated positions. Business owners who hold large amounts of company stock or a single sector position face outsized risk. Options hedging lets them reduce that risk without liquidating the position and potentially signaling concern to the market.

The key trade-off in every scenario is cost versus protection. A business that hedges every position all the time will see premium costs eat into returns. The goal is targeted protection during periods of elevated risk, not permanent insurance on every asset.

What are common misconceptions about options hedging?

The most damaging misconception is that options eliminate risk entirely. Options redistribute risk rather than remove it. A business that buys a protective put has traded some upfront cash for a defined floor. The risk has not disappeared. It has been restructured.

- Hedging is not market timing. A business does not need to predict where prices will go. It needs to decide how much loss it can tolerate and structure the hedge accordingly.

- No hedge is free. Protective puts cost premium. Collars cap upside. Index hedges carry basis risk. Every structure has a price, either in cash paid or in gains surrendered.

- Active management is not optional. A hedge placed in january and ignored until march may have decayed significantly or drifted far from its intended exposure. Hedging involves accepting a ceiling on upside or paying upfront premium, and active management is what keeps that trade-off working as intended.

- Underestimating premium costs is the most common practical error. Businesses that do not model the total cost of a hedging program over a full year often find it more expensive than anticipated.

Pro Tip: Before placing any hedge, write down the maximum loss you are willing to accept and the maximum premium you are willing to pay. Those two numbers define the structure you need. Do not let the math drive the decision after the fact.

Key Takeaways

Options hedging is a deliberate trade-off where businesses pay a defined cost, either in premium or capped upside, to set a floor on potential losses during periods of elevated market risk.

| Point | Details |

|---|---|

| Three core strategies | Protective puts, collars, and index hedges each solve a different risk problem at a different cost. |

| Premium cost drivers | Implied volatility, time to expiration, and strike distance determine what a hedge costs. |

| The Greeks matter | Delta, Gamma, Theta, and Vega must be monitored actively to keep a hedge working as intended. |

| Best timing for hedges | Hedge before binary events, to protect unrealized gains, or to manage concentrated positions without selling. |

| Risk is redistributed, not removed | Options shift which risks a business accepts. They do not eliminate exposure entirely. |

Why I think most businesses get options hedging wrong from the start

Most business owners approach options hedging the way they approach insurance: buy it, file it, forget it. That mindset is exactly why so many hedges fail to deliver. Options are not static contracts. They decay, they drift, and they respond to volatility in ways that change daily.

The businesses I have seen use hedging well treat it as an ongoing position, not a one-time purchase. They check their delta exposure regularly. They understand that a collar that made sense when implied volatility was low may look very different after a volatility spike. They also start small. Practicing on a single position before hedging an entire portfolio teaches you more about theta decay and delta drift than any theoretical explanation can.

The other thing worth saying plainly: hedging costs money. A business that expects to hedge for free, or to hedge without giving up some upside, is going to be disappointed. The value is in the certainty it provides, not in the returns it generates. Once you accept that trade-off clearly, the decision about when and how much to hedge becomes much more rational.

— Customer

How Morningoptions supports your hedging decisions

Knowing the theory of options hedging is one thing. Knowing which contracts to use, at what entry level, and on which underlying assets is where most business professionals get stuck.

Morningoptions delivers AI-powered options briefings every market morning, with ranked and specific contract ideas before the open. The platform's five-stage AI pipeline vets, scores, and explains each trade idea, covering both directional plays and hedging setups. The free daily briefing gives business professionals a fast read on the day's setups. The Pro tier at $89 per month adds a lunchtime scanner and an on-demand AI chat scanner for researching specific tickers. For business owners who want to act on hedging opportunities without spending hours on analysis, Morningoptions puts the research in your hands before the market opens.

FAQ

What is options hedging in simple terms?

Options hedging is the use of put or call contracts to limit potential losses on an asset a business already holds or plans to buy. It sets a predefined floor or ceiling on the asset's value for a specific period.

How much does it cost to hedge with options?

The cost depends on implied volatility, the time to expiration, and how close the strike price is to the current market price. Premium cost drivers mean that hedging during high-volatility periods is significantly more expensive than hedging during calm markets.

What is a protective put and when should a business use it?

A protective put gives the holder the right to sell an asset at a fixed price before expiry. Businesses use it to protect unrealized gains or to limit downside on a concentrated position without triggering a sale.

Do options eliminate risk entirely?

No. Options redistribute risk rather than remove it. A hedge trades one type of exposure, such as unlimited downside, for another, such as upfront premium cost or capped upside.

What are the Greeks and why do they matter for hedging?

The Greeks, specifically Delta, Gamma, Theta, and Vega, measure how an option's price responds to price moves, time decay, and volatility changes. Monitoring them actively keeps a hedge aligned with its intended level of protection as market conditions shift.