Tracking options trades systematically is the process of capturing and analyzing every trade using consistent rules and structured data fields to remove emotion and improve results. This discipline separates retail traders who grow accounts from those who repeat the same mistakes. Algorithmic trading now represents about 60% of all options volume on major U.S. exchanges as of Q2 2026. That number tells you something direct: the traders winning at scale are running rules-based systems, not gut instincts. Retail traders who adopt the same disciplined approach to options trade tracking methods gain the same structural edge, without needing a quant team.

What data fields should you track in an options trading journal?

Retail traders should track at least seven core fields per options trade to enable meaningful weekly review and risk assessment. Those fields are: underlying symbol, strategy tag, strike price, expiration date, number of contracts, premium in and out, and collateral reserved at open. Skipping even one of these fields creates blind spots that compound over time.

The Greeks deserve their own columns. Capturing Delta, Theta, and Vega at both entry and exit lets you diagnose exactly why a trade won or lost. Without Greek-based data, you are effectively blind to the mechanics driving your results. A trade that lost money because Theta worked against you requires a different fix than one that lost because Delta moved the wrong way.

Implied volatility rank (IV rank) at entry is one of the most underused fields in retail journals. IV crush following events can cause losses even when your directional call was correct. Logging IV at both entry and exit shows you whether you paid fair premium or overpaid, which directly informs your next setup.

Days to Expiration (DTE) at entry rounds out the core data set. Theta sellers often find optimal performance at 30–45 DTE, and historical DTE data from your own journal will confirm or challenge that benchmark for your specific strategies.

- Underlying symbol — identifies the asset and sector concentration

- Strategy tag — labels the structure (covered call, cash-secured put, iron condor, etc.)

- Strike price and expiration date — defines the contract and time horizon

- Contracts and premium — captures size and cost basis

- Collateral reserved — prevents risk overconcentration across simultaneous positions

- Greeks at entry and exit — Delta, Theta, Vega for diagnostic review

- IV rank and DTE at entry — calibrates volatility timing and time decay exposure

Pro Tip: Add a single "rule adherence" column with a yes or no value for every trade. This binary check takes five seconds to fill in and becomes your fastest tool for spotting behavioral drift during weekly reviews.

What tools and methods work best for capturing trade data?

The right tool for systematic options trading depends on your volume and technical comfort. Three categories cover most retail traders: manual spreadsheets, dedicated trading journal apps, and automated broker data import tools.

| Method | Best for | Key advantage | Main limitation |

|---|---|---|---|

| Spreadsheet (Excel, Google Sheets) | Traders who want full control | Fully customizable formulas and layouts | Manual entry creates friction and errors |

| Dedicated journal apps | Traders who want structure out of the box | Pre-built fields for Greeks, IV, and P&L | Less flexibility for custom strategy tags |

| Automated broker import | High-volume traders | Eliminates manual entry errors | Requires broker API access or CSV export |

![]()

Manual entry forces you to re-read every trade before logging it. That friction is actually useful early in your development because it builds pattern recognition. Automated import removes friction but also removes that forced review moment. The best approach for most active retail traders is automated import combined with a manual notes field where you record your reasoning and rule adherence.

Setting up a spreadsheet template correctly matters more than which platform you use. Build separate tabs for entry data, exit data, and a summary dashboard. Use formulas to auto-calculate P&L, net premium collected, and collateral utilization. Lock the column headers so the structure never drifts.

- Create a "Trades" tab with one row per trade leg, not per position

- Build an "Exit" tab that pulls entry data by trade ID and adds close fields

- Add a "Weekly Review" tab that filters by strategy tag, DTE bucket, and IV rank tier

- Include a "Rule Breaks" tab that auto-populates from your yes or no adherence column

Pro Tip: Set a recurring calendar block every Sunday for 20 minutes to run your weekly review. Traders who skip this step lose the compounding benefit of their own data. The review is where the tracking pays off.

How to build a systematic options trade tracking routine

A repeatable workflow is what turns a journal from a record into a coaching tool. The process has four steps, and each one feeds the next.

Step 1: Record at entry. Log all seven core fields the moment you open a position. Add Delta, Theta, Vega, IV rank, and DTE. Write one sentence explaining why you took the trade and confirm your rule adherence with a yes or no. This takes under three minutes and creates the foundation for every future analysis.

Step 2: Log at exit. Record your closing premium, final P&L, IV at exit, and your reason for closing. "Hit profit target," "stopped out," and "expired worthless" are three different outcomes that require different analysis. Lumping them together hides the signal.

Step 3: Run your weekly review. Weekly review of tracked trades focusing on strategy type, DTE, IV rank, and rule adherence helps identify clusters and opportunities for improvement. Sort your trades by strategy tag and look for patterns. A string of losses on iron condors during high IV weeks tells you something specific about your entry timing.

Step 4: Filter for behavioral drift. Rule break flags quickly expose behavioral drift that often leads to losses. Pull every trade where you logged a "no" on rule adherence and calculate the average P&L for those trades versus your compliant trades. Most traders find the gap is larger than they expected.

Common mistakes that undermine the whole system:

- Skipping collateral tracking on cash-secured puts, which masks true capital at risk

- Logging a roll as one event instead of two, which distorts cumulative P&L

- Waiting until the weekend to log entry data, which causes memory errors on Greeks and reasoning

- Using vague exit reasons like "felt wrong" instead of specific rule-based criteria

Advanced tracking techniques that sharpen your edge

Sophisticated options trade tracking goes beyond filling in fields. The traders who extract the most from their journals use a few specific techniques that most retail guides skip entirely.

Track rolls as two linked events. Most beginners treat a roll as one event, but recording it as a close and a new open maintains true P&L visibility. This matters because a roll that collects additional premium can still represent a losing position when you account for the original loss. Linking the two entries by a shared position ID lets you calculate cumulative P&L across the full lifecycle of a trade.

Use IV rank to calibrate entry timing. Logging IV rank at entry across dozens of trades reveals your personal volatility sweet spot. You may find that your iron condors perform well when IV rank is above 40 but break down below 30. That insight only emerges from tracked data, not from reading general options theory.

Apply Delta hedging principles to your journal analysis. Institutional traders treat options primarily as volatility bets rather than directional plays. Reviewing your Delta at entry across all losing trades tells you whether your losses come from directional exposure or volatility mispricing. That distinction changes how you adjust your strategy.

- Record IV rank and IV percentile separately at entry, since they measure different things

- Tag each trade with a market regime label (trending, range-bound, high volatility) to identify which setups perform best in which conditions

- Use a "lesson learned" field for every losing trade, limited to one sentence, to build a personal error catalog

Pro Tip: After 50 trades, filter your journal by your top three performing strategy tags and calculate average DTE, average IV rank at entry, and average Delta. Those three numbers define your personal edge. Build your future setups around them.

A written trading plan tied directly to your journal creates a feedback loop that most retail traders never build. The plan defines the rules. The journal measures whether you followed them. The weekly review closes the loop.

Key Takeaways

Tracking options trades systematically requires consistent data capture, Greek-level diagnostics, and weekly review to turn raw trade records into a repeatable edge.

| Point | Details |

|---|---|

| Log seven core fields at entry | Underlying symbol, strategy tag, strike, expiration, contracts, premium, and collateral are the minimum for meaningful analysis. |

| Track Greeks and IV at entry and exit | Delta, Theta, Vega, and IV rank reveal why trades win or lose, not just whether they did. |

| Record rolls as two linked trades | Closing and reopening a position as separate entries preserves true cumulative P&L visibility. |

| Run a weekly review by strategy and rule adherence | Filtering by strategy tag and rule breaks exposes behavioral drift before it erodes your account. |

| Use IV rank history to find your edge | Patterns in your own IV rank data at entry reveal the volatility conditions where your strategies perform best. |

Why most traders track too little, too late

The traders I see struggle most with systematic tracking are not lazy. They are busy. They take the trade, move on, and plan to "catch up on the journal later." Later never comes with the same detail that the moment of the trade does. By Sunday, the reasoning behind a Wednesday entry is a blur.

The real cost is not the missing data. The real cost is the missing feedback loop. Systematic methodology is the meaningful divide between retail traders and institutional desks, not superior luck or intuition. Institutions do not rely on memory. They rely on records. Every position has a timestamp, a rationale, and a post-trade review. Retail traders who build that same habit close the gap faster than any strategy upgrade could.

Tracking Greeks and collateral separately feels like extra work until the first time it saves you from overexposing yourself on a week when four cash-secured puts expire simultaneously. That moment changes how you think about the journal. It stops being a chore and starts being a risk management tool.

The binary rule check is the single highest-leverage habit in this entire system. A disciplined journal with a binary rule check reduces behavioral drift and prevents the common scenario of repeated small rule breaks that erode accounts. Yes or no. Compliant or not. That one column, reviewed weekly, acts as your personal coach. It does not care about your feelings. It just shows you the data.

— Customer

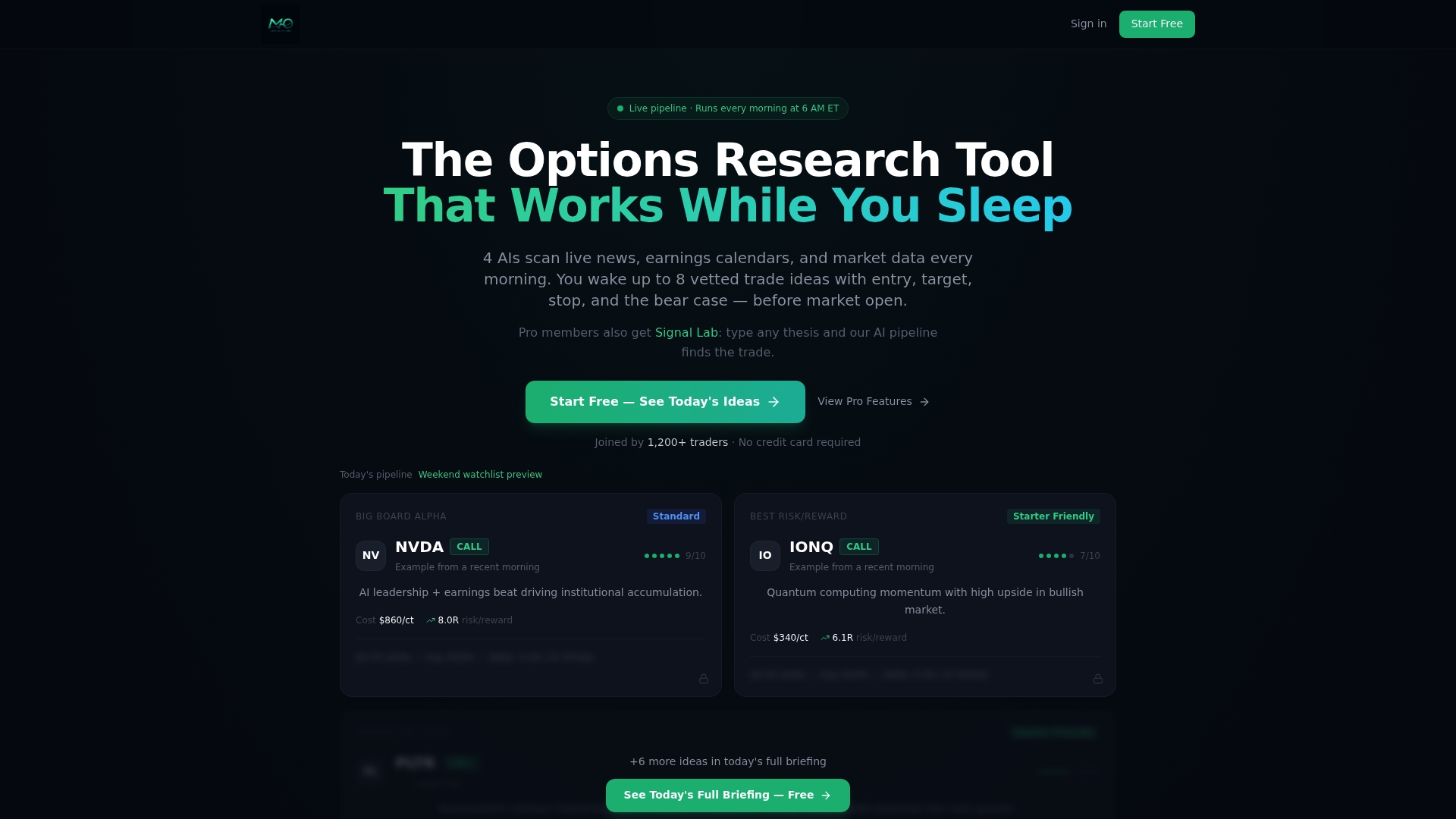

Morningoptions delivers the pre-market edge your journal needs

Systematic tracking tells you what happened. Morningoptions tells you what to look at before the open.

Morningoptions runs a five-AI pipeline every market morning to vet, score, and rank specific contract ideas with entry levels. You get ranked trade ideas before the market opens, not vague commentary after the fact. Each briefing gives you the raw material to populate your journal with high-quality setups from the start. The free daily briefing covers the core ideas. The Pro tier at $89/mo adds a lunchtime scanner and an AI chat scanner for researching tickers on demand. When your tracking system is already in place, Morningoptions slots directly into your entry workflow and gives you more to analyze, not more noise to filter.

FAQ

What is systematic options trade tracking?

Systematic options trade tracking is the disciplined, rules-based process of recording and analyzing every trade using consistent data fields. It removes emotional decision-making and creates a feedback loop for continuous improvement.

What are the most important fields to log in an options journal?

The seven core fields are underlying symbol, strategy tag, strike price, expiration date, number of contracts, premium in and out, and collateral reserved. Adding Greeks and IV rank at entry and exit makes the journal diagnostic rather than just descriptive.

How do you track a rolled options position?

Record a roll as two linked entries: one closing trade and one opening trade, connected by a shared position ID. This preserves accurate cumulative P&L and shows whether the roll actually reduced risk or delayed a loss.

How often should you review your options trading journal?

A weekly review is the minimum effective frequency. Filtering by strategy tag, DTE bucket, IV rank, and rule adherence each week exposes performance clusters and behavioral drift before they become costly patterns.

Why does IV rank matter in options trade tracking?

IV rank at entry reveals whether you paid fair or inflated premium. Logging it consistently across trades shows the volatility conditions where your strategies perform best, which is data you cannot get from theory alone.